For many businesses, MCA compliance still feels like a year-end filing activity. Accounts are closed. Auditors ask for records. Finance teams rush to collect documents. IT teams search for logs. Then everyone hopes the audit report stays clean. That approach does not work.

MCA Compliance FY 2026–27 is not just about filing AOC-4, MGT-7, board resolutions, or annual returns on time. It is now about proving that your financial data, accounting systems, and digital records have remained traceable throughout the year.

What does the MCA Compliance FY 2026-27 require?

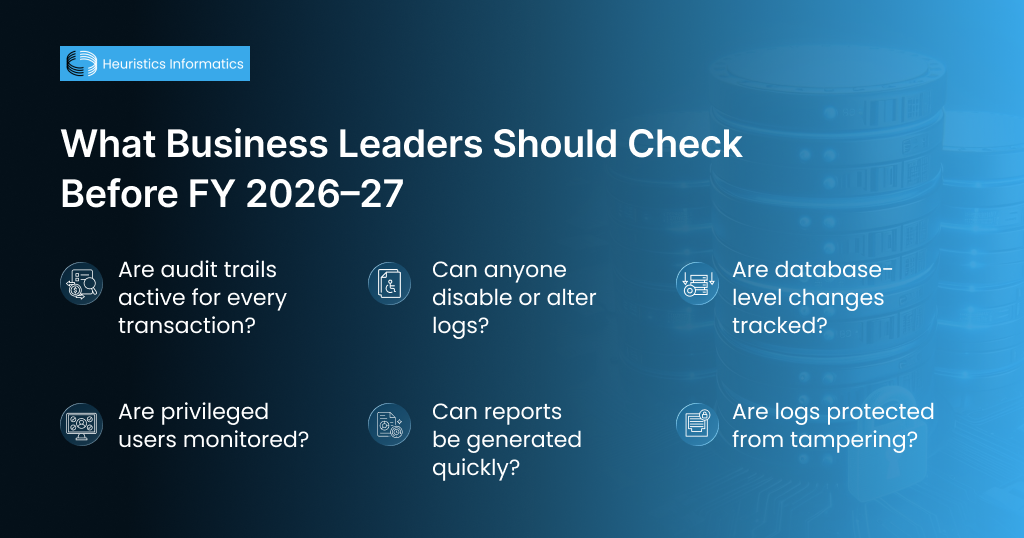

MCA Compliance in FY 2026–27 requires companies to maintain accurate books of account, statutory filings, and traceable digital financial records. For companies using accounting software, this includes continuous audit trail or edit log functionality that records transaction changes and supports auditor verification. The Ministry of Corporate Affairs has made audit trail compliance a serious governance requirement. If your company maintains books of account in accounting software, that software must record an audit trail or edit log for every transaction. It must also capture changes made in books of account and ensure that the audit trail cannot be disabled. ICAI’s revised implementation guidance confirms that audit trail reporting sits under Rule 11(g) of the Companies (Audit and Auditors) Rules, 2014, and links directly to the Companies (Accounts) Rules requirement for accounting software.

The audit trail requirement isn’t new, MCA introduced it through an amendment to Rule 3(1) of the Companies (Accounts) Rules, 2014, and it became mandatory from April 1, 2023. But FY 2026–27 is the year enforcement gets serious. Auditors are now expected to actively verify and report on audit trail compliance, not just take a company’s word for it.

Here’s what the rule actually says, in plain business language:

- Every company using accounting software to maintain its books must use software with a built-in audit trail feature.

- The software must create an edit log for every transaction, who changed it, what changed, and when.

- This edit log must run continuously through the financial year. It cannot be switched off, paused, or bypassed at any point.

- Auditors must confirm this in their report. If they can’t, they’re required to qualify it.

MCA is essentially asking every company to install one, permanently, and without an off switch.

Why does this rule exist?

Under Section 128 of the Companies Act, 2013, the intent is straightforward: stop silent data manipulation. For years, companies could alter financial entries after the fact with no record of the change. Numbers could shift quietly between the transaction date and the balance sheet date, and nobody outside the finance team would know.

That gap created real risk, for investors, for lenders, for regulators, and honestly, for company leadership too. An audit trail closes that gap. It doesn’t just protect the regulator’s interest. It protects yours, especially if a fraud investigation, lender due diligence, or internal dispute ever puts your books under scrutiny.

What are the penalties for MCA Compliance failures?

Let us talk numbers, because that is what tells the real story.

- Under Section 128(5), non-compliance can attract a fine ranging from ₹50,000 to ₹5,00,000 for the company.

- Directors, CFOs, and other officers responsible for compliance face personal liability, with fines in the same ₹50,000 to ₹5,00,000 range, and in cases of willful default, imprisonment of up to one year.

- Auditors who fail to flag non-compliance face penalties under Section 147(2), ranging from ₹25,000 to ₹5,00,000, or up to four times their remuneration, whichever is lower.

- A qualified audit report isn’t just an internal embarrassment. It becomes public record, and it invites further MCA scrutiny.

What catches most businesses off guard is that it is not a one-time penalty you pay and move past. If your systems don’t maintain a continuous, tamper-proof audit trail, every financial year without one is a fresh exposure. If you multiply that risk across every ERP instance, every database, every finance application running in your enterprise, you start to see why this deserves boardroom attention, and not just a line item in the compliance checklist.

Why Accounting Software may not be enough for MCA Compliance?

Most businesses assume this rule lives entirely inside their accounting or ERP application. Enable a setting, tick a box, done. That is where the real gap opens up.

Your accounting software sits on top of a database. Oracle, SQL Server, or another enterprise database platform holds the actual transaction data. And here’s the uncomfortable truth: a privileged user with direct database access, a DBA, a systems administrator, even a well-meaning developer — can bypass the application layer entirely and edit records straight at the database level.

If that happens, your accounting software’s audit trail sees nothing. The edit log stays clean. But your data isn’t. This is exactly the blind spot regulators, auditors, and increasingly, forensic investigators are starting to ask about. Application-level audit trails answer “what changed in the software.” They don’t answer “what changed in the database.” And for MCA compliance to actually hold up under scrutiny, both questions need clear answers.

Why Database Activity Monitoring matters for MCA Compliance

Database activity monitoring gives your business visibility into what is happening inside your data layer. It works below the accounting application, watching every query, every login, every privileged action directly at the database engine. It doesn’t rely on the accounting software to log a change correctly. It captures the activity at the source, independent of whether someone tried to go around the application. More importantly, it builds a stronger evidence layer for auditors, compliance teams, and leadership.

This matters because fraud, error, and data manipulation often hide in places where normal dashboards do not look. The Association of Certified Fraud Examiners studied 2,402 occupational fraud cases across 143 countries and territories in its 2024 Report to the Nations. The report highlights how internal controls influence fraud losses, and notes that the presence of every control studied was associated with lower fraud losses.

MCA compliance checklist. How to build audit readiness

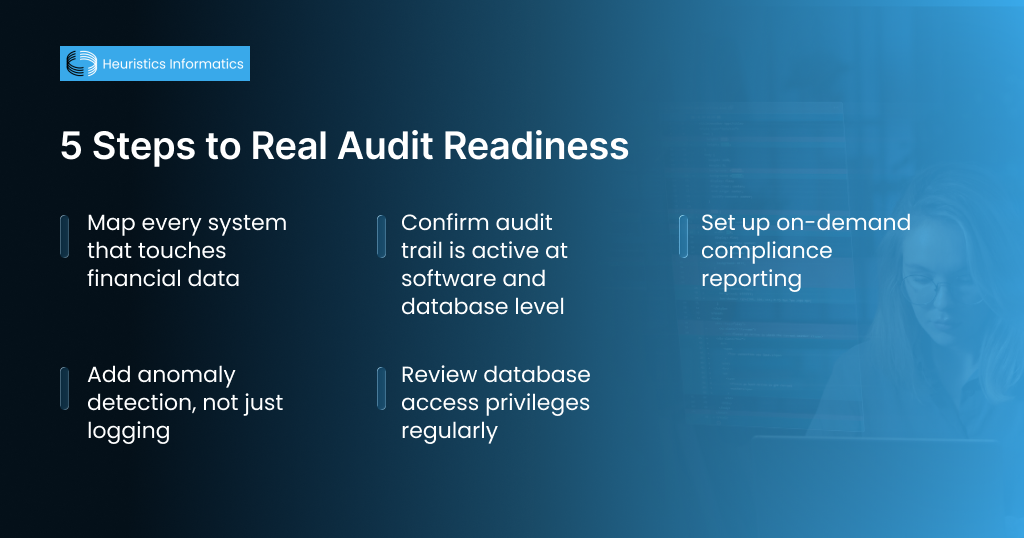

Audit readiness isn’t a scramble you do in September before your AGM. It’s a posture you maintain all year. A few practical steps make the difference:

- Map every system that touches financial data. Your ERP, your database, your integrations, list them all. Compliance gaps hide in the systems nobody thinks to check.

- Confirm audit trail is active at both layers. Application-level logging and database-level monitoring need to run together, not one instead of the other.

- Set up compliance reporting that’s ready on demand. If your auditor asks for a change log covering the last six months, you should be able to produce it in minutes, not days.

- Add anomaly detection, not just logging. A record of changes is useful. A system that flags unusual patterns, say, a bulk edit to closed-period transactions at 2 AM, is what actually prevents fraud before it becomes a headline.

- Review access privileges regularly. Many audit trail failures trace back to over-provisioned database access that nobody remembered to revoke.

Regulatory compliance, done well, stops being a once-a-year fire drill. It becomes a byproduct of good data governance. That shift is exactly what separates companies that sail through their statutory audit from companies that spend October explaining gaps to their board.

How does Oracle AVDF support MCA Compliance and reduce Audit Trail penalty risk?

Oracle AVDF does not replace compliant accounting software. Your accounting application must still meet MCA’s audit trail requirements.

However, Oracle AVDF strengthens the control environment around that application and its database. It helps your business in five practical ways.

Centralized Audit Trail Visibility

Oracle AVDF consolidates audit data across databases and related systems. This gives your finance, IT, security, and audit teams a single place to review database activity.

That is valuable when your business runs multiple applications across different departments, locations, or business units.

Tamper-Resistant Audit Evidence

Audit trail penalties often arise when companies cannot prove that records were maintained properly. Oracle AVDF stores collected audit data in a secure repository, helping protect audit evidence from tampering.

This gives auditors more confidence in the integrity of the evidence.

Privileged User Monitoring

Many serious data risks come from privileged users. These users may be DBAs, developers, support teams, consultants, or power users.

Oracle AVDF helps monitor sensitive database activity and privileged access. That matters because privileged access can bypass normal application controls.

Anomaly Detection and Alerts

Compliance is not only about post-event reporting. It is also about early warning.

Oracle AVDF supports monitoring, reporting, and alerting of anomalous database activity. Oracle documentation also notes that AVDF reports any access to sensitive data stored in the database.

This helps your team identify unusual access patterns before they become audit exceptions.

Faster Compliance Reporting

Audit teams often spend days or weeks collecting logs, screenshots, reports, and explanations. Oracle AVDF supports automatically generated reports on collected audit and network event data. Reports can also be saved or scheduled in PDF or Excel format.

That makes compliance reporting faster, cleaner, and easier to defend.

Why does FY 2026–27 need a stronger compliance architecture?

MCA compliance FY 2026–27 has already started. If your accounting software has audit trail enabled but your underlying database doesn’t have independent monitoring, you have a gap, and gaps like this tend to surface at the worst possible time, mid-audit, with a qualified report already on the table.

The fix isn’t complicated. It’s a matter of extending your audit trail from the application layer down to the database layer, where the real financial data actually lives. Do that, and audit trail penalties stop being a risk you manage and start being a risk you’ve already closed.

PwC’s Global Compliance Survey 2025 collected feedback from 1,800 executives across 63 countries and found that technology is a top compliance priority, with cybersecurity, data protection, and privacy cited as key priorities by more than half of respondents.

At the same time, the cost of digital weakness is increasing. IBM’s 2024 data breach research reported that the global average cost of a data breach reached $4.88 million, a 10% increase over the previous year. These numbers may not directly represent MCA penalties. But they show the larger boardroom reality.

Data integrity is now a business risk, not just an IT risk. For FY 2026–27, your business cannot afford a loose compliance stack. You need systems that can prove control, not just claim control.

How do HIPL and Oracle AVDF help you stay audit-ready?

At HIPL, we’ve spent over three decades helping enterprises across manufacturing, finance, healthcare, energy, and public sector organizations get their Oracle environments not just running, but genuinely secure and audit-ready. Oracle Audit Vault and Database Firewall (Oracle AVDF) sits at the center of that work, and it’s built precisely for the gap most MCA compliance conversations miss.

Oracle AVDF gives you continuous, database-level activity monitoring that operates independently of your accounting or ERP software. It captures every privileged action, every query, every login attempt, and every change made directly at the database, creating a genuinely tamper-proof audit trail that no application-layer bypass can quietly slip past. Paired with built-in anomaly detection, it flags unusual database behavior in real time, so your team catches risk before it becomes a finding in someone else’s audit report.

For CIOs and finance leaders navigating MCA Compliance FY 2026–27, HIPL brings the Oracle expertise to implement AVDF correctly the first time, mapped to your existing Oracle EBS, Fusion, or database landscape, configured for compliance reporting that’s audit-ready on demand, and backed by our managed services team for ongoing monitoring and support. We don’t just help you check a compliance box. We help you build a database security posture that holds up under real scrutiny, protects your data integrity, and gives your board one less thing to worry about at audit time.

If audit trail penalties are a risk on your radar, let us talk about closing that gap properly, at the database layer, where it matters most.

Frequently Asked Questions

What is MCA Compliance FY 2026–27?

MCA Compliance FY 2026–27 refers to the statutory filings, governance records, disclosures, audit reports, and digital record-keeping requirements that Indian companies must manage for the financial year 1 April 2026 to 31 March 2027.

What are audit trail penalties?

Audit trail penalties are compliance consequences that may arise when a company fails to maintain proper audit trail records in its accounting software or cannot prove that the audit trail remained active, complete, and tamper-proof.

Is Oracle AVDF mandatory for MCA compliance?

Oracle AVDF is not mandatory under MCA rules. However, it helps strengthen database activity monitoring, audit readiness, regulatory compliance, anomaly detection, and compliance reporting.

Can Oracle AVDF replace accounting software audit trail requirements?

No. Oracle AVDF does not replace the audit trail feature required in accounting software. It adds a powerful database-level monitoring and evidence layer around your enterprise systems.

Who should evaluate Oracle AVDF?

CIOs, CFOs, IT heads, compliance leaders, audit teams, CISOs, department heads, and businesses running critical databases should evaluate Oracle AVDF as part of their compliance and security architecture.